You’re paying for a CRM, social marketing programs, a Google search account, a video platform, and maybe an AI lead qualification service. Your collection of loan officer marketing tools runs between $400 and $700 a month. You’ve done the work. And yet when someone asks how your marketing is performing, you hesitate.

Not because business is bad. Because you genuinely can’t connect a funded loan back to any specific tool.

This is the quiet problem underneath most loan officer marketing stacks. Tools are easy to buy. A marketing plan that builds compounding demand generation, produces higher-intent borrowers, and gets smarter over time is something else entirely.

Key Takeaways

- Most loan officers pay for multiple marketing tools that operate independently, each optimizing for its own metric rather than the outcome that matters: funded loans.

- Having several loan officer marketing tools is not the same as having a marketing plan. Tools are inputs; a plan is the system that coordinates them toward a shared goal.

- Fragmented marketing stacks generate activity — impressions, clicks, and form fills — without building compounding demand generation over time.

- A real loan officer marketing plan has a goal, a coordinated channel strategy, a learning loop, and results that compound the longer the plan runs.

- The LOs building predictable pipelines are not running more tools. They’re running a system where the tools work together toward one outcome.

The Average Loan Officer’s Marketing Stack — And What It Actually Costs

Most loan officers piece together their marketing from multiple vendors. The typical stack looks something like this:

- A CRM for contact management and email sequences: $50–$150/month

- Social marketing programs across Facebook and Instagram: $150–$300/month in spend

- Google search programs targeting bottom-of-funnel borrowers: $150–$300/month

- A video or content creation platform: $30–$100/month

- An AI lead qualification or calling service: $100–$300/month

Totaled up: $480 to $1,150 per month across tools that each operate in isolation.

The CRM doesn’t know what your Google programs are producing. Your AI calling service doesn’t know which channel the lead came from. Your video content runs disconnected from your demand generation programs.

Each tool optimizes for its own metric. None of them is optimizing for funded loans.

What’s the Difference Between Loan Officer Marketing Tools and a Marketing Plan?

A tool does one thing. A plan does everything in the right order.

A marketing plan is a system that takes a specific goal — grow a borrower pipeline in a defined market, build brand visibility with move-up buyers, re-engage a past client database — and executes a coordinated set of activities across every relevant channel. It learns from the results. It adjusts over time.

Tools are inputs to a plan. Without a plan directing them, they generate noise.

Think about what a marketing director at a lending company actually does. They don’t set up channels and walk away. They decide which channels fit the goal. They sequence messaging so that a borrower who clicks a Google search program gets followed up by the same system building visibility on social platforms. They analyze which programs produce higher-intent borrowers and reallocates budget toward what’s working. They build audiences that compound over time so every new program starts smarter than the last.

Loan officers who try to do all of that manually while also closing loans end up doing none of it well. Something always falls through. Usually it’s the marketing.

Why Fragmented Tools Create Activity, Not Demand Generation

The core problem with most loan officer marketing stacks: nothing talks to anything else.

A borrower searches “mortgage rates near me” on Google, clicks through, and doesn’t fill out the form. They leave. In most setups, that’s where the trail ends. The impression is spent. The click is gone. The borrower is unreachable.

A borrower who scrolls past your content on Instagram hasn’t visited your website, so your AI calling service doesn’t know they exist. Your CRM doesn’t have them. The opportunity never makes it into your pipeline.

The big portals aren’t running five separate tools. They’re running one coordinated machine. Every impression, click, and engagement feeds the same intelligence layer. The system learns. It adapts. It gets better at finding borrowers who close, not just borrowers who fill out forms. Local loan officers pay to compete in the same attention market. A patchwork of disconnected tools isn’t the same game.

The result is activity without compounding. Spend without learning. Each month largely starts from zero.

One loan officer who recognized this dynamic made a deliberate shift: from disconnected programs to a single, coordinated demand generation platform with Evocalize. Over 12 months, he generated approximately 70 loan applications from $5,100 in total marketing spend — an estimated 5x return. His assessment after more than a year of consistent programs: “It’s the best marketing money that I spend.”

What a Real Marketing Plan Looks Like for a Loan Officer

A real loan officer marketing plan doesn’t run for 30 days and reset. It’s a rolling system that lives with your business over time.

Here’s the structure:

Goal. Not “run programs on Facebook” but “build a borrower pipeline in a specific market, focused on a defined buyer type.” The goal determines the channel strategy, the messaging, and what success looks like.

Channel coordination. Paid search captures borrowers in active research mode. Social demand generation builds brand recognition with your ideal borrower profile before they start searching. Database marketing keeps past clients in your orbit. Direct mail reinforces your digital presence in your area. All of it runs toward the same outcome under one plan.

Learning loop. Every program produces signals: lead quality, response rates, cost per higher-intent lead. A smart plan uses that data to improve the next program. It adjusts budget toward what’s working. It reaches borrowers who showed interest earlier. Borrower quality improves as the platform learns your specific market.

Compounding returns. The longer the plan runs, the more valuable it becomes. Local recognition builds. The system learns what a strong borrower looks like for your book of business and produces more of them.

Another loan officer experienced exactly this shift. Moving from a disconnected stack to an integrated demand generation platform, he generated two pre-approvals totaling approximately $1.5 million in volume within the first three months, including a hard money referral worth approximately $900,000. His read on it: “If one of those closes, I’ve paid for Evocalize for a whole year.”

The difference between these results and the typical disconnected stack is not budget. It’s the system.

How to Audit Your Own Loan Officer Marketing Stack

Before adding another subscription, ask these four questions about the tools you already have:

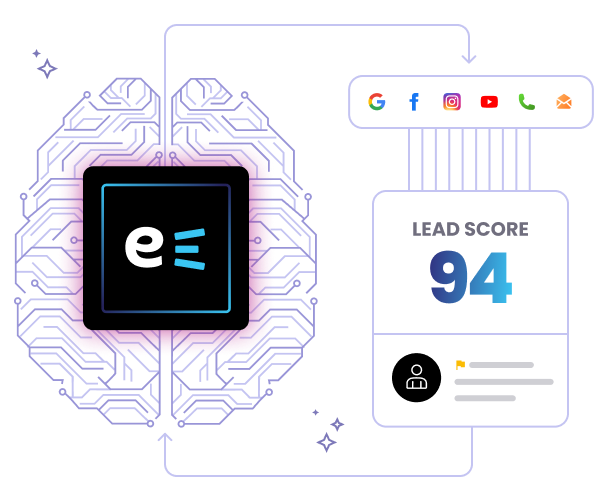

- Can you trace a funded loan back to a specific marketing activity? If not, your programs are generating activity, not demand. A real marketing plan has attribution across channels, not just impressions and clicks.

- Do your tools share data with each other? If your Google programs don’t inform your CRM, and your CRM doesn’t inform your AI follow-up service, your marketing isn’t compounding. Each month starts fresh.

- Does your marketing run when you’re busy closing? Most loan officers market when business is slow and stop when it picks up. That cycle keeps the pipeline unpredictable. A real plan runs as a continuous growth engine. That’s what separates reactive marketing from a system that builds over time.

- Are you reaching borrowers before they’re ready, or only when they already are? According to Zillow’s 2025 Consumer Housing Trends Report, 22% of buyers spend six months or more actively researching before purchasing. Loan officer marketing tools that only capture people ready to fill out a form right now are missing the majority of the market.

If your current stack can’t answer yes to most of these, it’s a collection of subscriptions, not a marketing plan.

Marketing Campaign vs. Marketing Plan: What Loan Officers Need to Know

FAQs

How many loan officer marketing tools do I actually need?

The number of tools matters far less than how they work together. Loan officers running three integrated programs under a coordinated plan consistently outperform those paying for six disconnected subscriptions. Before adding a new platform, ask whether your existing tools are working as a system: sharing data, coordinating touchpoints, and building compounding demand generation over time. Less is more when the tools are actually aligned.

What’s the difference between a loan officer marketing program and a marketing plan?

A marketing program is time-limited. It runs for 30 or 60 days, ends, and the learning largely resets. A marketing plan is continuous. It runs while you’re closing, learns what works in your specific market, and compounds with every program cycle. Loan officers who run one-off programs often feel like they’re starting over every quarter. Loan officers who run plans watch borrower quality and pipeline predictability improve the longer the system runs.

How do I know if my loan officer marketing tools are actually generating business?

The clearest signal is whether you can connect a funded loan back to a specific marketing source. If you can’t, your tools are generating activity, not demand generation. Look for platforms that provide attribution across channels, not just vanity metrics like impressions and clicks. The metric that matters is borrower quality: are the people entering your pipeline becoming pre-approvals and funded loans?

How long does it take to see results from a loan officer marketing plan?

Meaningful pipeline momentum typically develops over 6 to 12 months of consistent, always-on programs. Digital marketing for loan officers compounds over time. The longer the system runs, the better it understands your market and the stronger your results. Loan officers who stop at 60 or 90 days are often weeks away from the compounding that makes the investment worthwhile. Consistency, not volume, is what separates LOs who build predictable pipelines from those who feel like they’re always starting over.

Stop Buying Tools. Start Running a Plan.

Evocalize is a digital marketing growth engine built for mortgage loan officers and the lending companies that support them. It’s not another tool to add to your stack. It’s the platform that replaces the stack with a coordinated marketing plan that learns, adjusts, and compounds over time.

One of Evocalize’s lending partners has generated more than $1 billion in loan applications with a 300% return on marketing investment. Not by buying more tools. By running an integrated demand generation system across every channel that matters.

If your loan officer marketing tools aren’t answering “is this building my business?”, the answer isn’t another subscription. It’s a plan.